Full-reserve banking was tried out in the UK and US in the 19th century. It is assuring that macroeconomic indicators pointed mainly upwards after the reforms were implemented. Although it is hard to associate the positive developments directly with full-reserve banking experiments, at least it should be clear that they did not have a destabilizing impact on the economy.

This article summarizes some of the key points made in my Ph.D. dissertation “Full-Reserve Banking: Separating Money Creation from Bank Lending” (University of Helsinki).

Full-reserve banking was tried out in the 19th century. At the time, private bank-issued notes were the prevailing means of payment. Today, it is hard to imagine that each bank would issue their own notes, but that was the case two centuries ago. In the UK, the Bank Charter Act of 1844 prohibited private money creation by requiring that bank-issued notes should be fully backed by government money or gold. The National Acts of 1863 and 1864 implemented full-reserve banking in the US. The experiments were never actually abandoned, but banks were able to circumvent regulation by issuing deposits instead of notes. This effectively undermined the reform, and this is how we ended up to our current monetary system. Nevertheless, the government (including also the central bank) has maintained a monopoly on issuing notes ever since.

Now is the time to experiment full-reserve banking with electronic money as well. The reform would prohibit private money creation, at least in the sense that the government would not guarantee repayment or par clearance of private monies or money-like assets. This would mean that there would be no more deposit guarantee and the central bank would not act as the lender of last resort for private actors. Consequently, banks could not create new money simultaneously when making loans, but they would have to acquire their funding before lending it out. In other words, banks would simply function as any other financial institution functions today.

Fiscal capacity expanded significantly

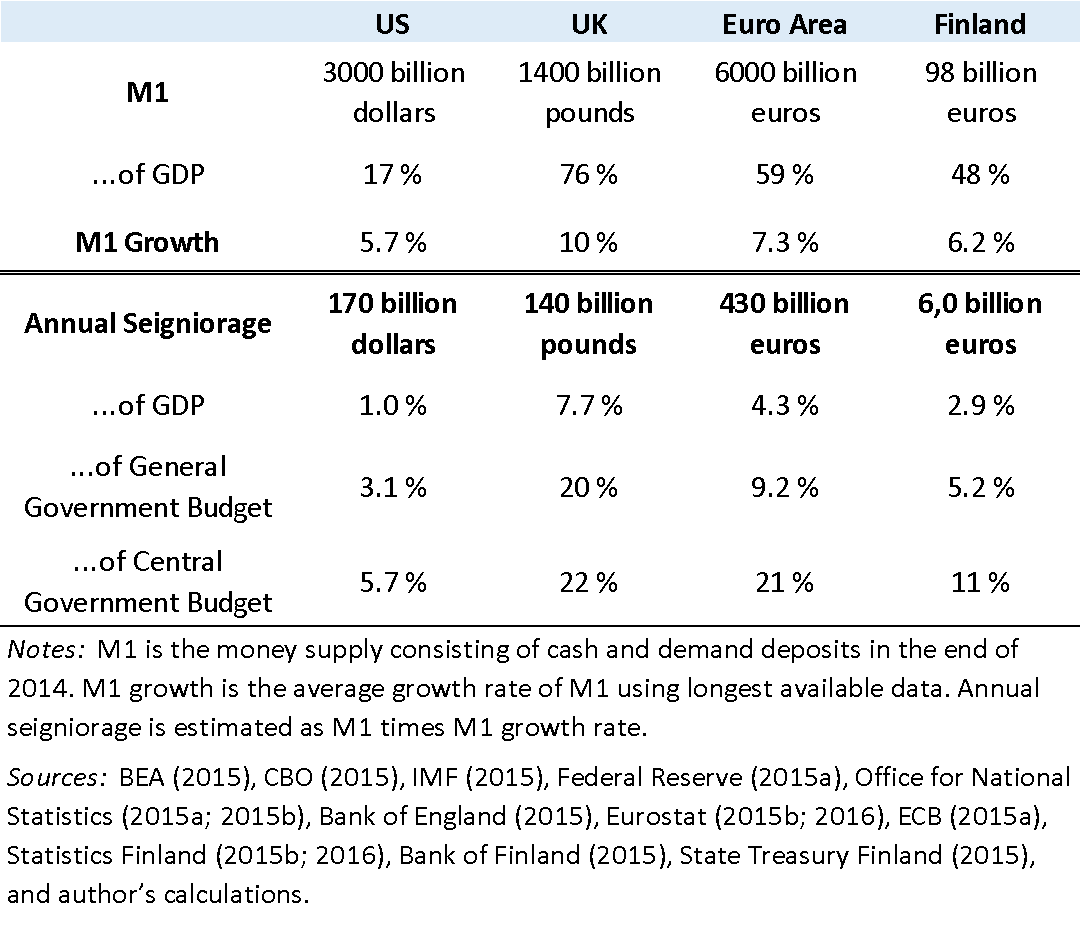

I argue that full-reserve banking could also significantly expand the government’s’ fiscal capacity. Assuming the M1 money supply continues its historical growth rate, I have calculated that full-reserve banking would generate over 400 billion euros each year, on average, in the euro area, . The seigniorage revenue is 4 % of euro area GDP or over 20 % of central government budgets of the euro area member states. It is hard to imagine that such a hike in government’s fiscal capacity could be achieved with any other reform.

Figure 1. Average annual seigniorage revenue from full-reserve banking

Similar findings are also supported by simulations with a Stock-Flow Consistent macroeconomic model. I find that under full-reserve banking, unlike in other cases, money creation leads to a permanent reduction in consolidated government debt, thus increasing the fiscal space of the government.

Towards a partial implementation of full-reserve banking

Fears that full-reserve banking would cause credit crunches or excessively volatile interest rates (e.g. Mitchell 2015b; Kregel 2012; Independent Commission on Banking 2011; Bossone 2001; 2002; Goodhart 1993) are not well justified. Indeed, most detailed proposals based on public money – such as sovereign money – include flexible elements that would make it relatively easy to avoid them. The observation is also supported by simulations with the Stock-Flow Consistent macroeconomic model.

Perhaps the most convincing critique against full-reserve banking is that near-monies (non-cash assets that are highly liquid) could undermine the reform, as happened in the 19th century. That is, it is possible that people would prefer private money-like assets rather than sovereign money as the former might offer a positive return — despite not being guaranteed by the government. Personally, I don’t believe it would happen, but, of course, it is a possibility.

Only a new experiment with full-reserve banking could provide an answer to that question. Nevertheless, complete adoption of full-reserve banking seems unlikely in any country in the near future as the Prime Minister of Iceland is not anymore actively supporting it and the reform was recently turned down in a referendum in Switzerland.

Due to technological progress and technocratic developments, however, partial adoption of full-reserve banking in the form of “digital cash” (a.k.a. deposited currency or central bank digital currency) seems quite likely. Obviously, the benefits would not be as big as with complete adoption, but also the risks of failure are clearly smaller. Who knows, perhaps small steps will eventually lead to a complete transition to a full-reserve banking system.

Patrizio Lainà’s Ph.D. thesis is freely available here.

It is possible to create money completely naturally. The use of credit cards with their debt paid off in 30 days does it. New money should be created in NO other way. This would eliminate money system caused inflation through the obver production of new money.

Dear Patrizio, in your calculation you forget to include the one-time bonus from the conversion of all pre-existing bank deposits into the new token. This is a sum officially calculated as 50% of GDP n many countries. For example, in Italy it is about one trillion euro. This comment is just for reinforcing your argument. Here I have published your article in Italian: http://centralerischibanche.blogspot.com/2018/11/e-ora-di-sperimentare-le-banche-riserva.html

“Perhaps the most convincing critique against full-reserve banking is that near-monies (non-cash assets that are highly liquid) could undermine the reform, as happened in the 19th century. That is, it is possible that people would prefer private money-like assets rather than sovereign money as the former might offer a positive return — despite not being guaranteed by the government.”

That depends entirely on how rigorously government enforces full reserve. To illustrate, if all bank statements, web sites etc associated with privately issued near-money had something in bold type saying “In the event of this bank or institution failing, government will not bail out depositors”, that would have a dramatic effect. I.e. depositors would flee to safe accounts (i.e. accounts where their money is lodged at the central bank), or they’d accept that they were not depositors in the normal sense of the word, but were in fact shareholders in the bank / institution, and hence that what was in their possession was shares rather than money.

Put another way, the shysters, hustlers, banksters and so on who work in the World’s financial centres are constantly trying to portray their liabilities as being as good as central bank money, and constantly bribe politicians into passing legislation that enables them to do that. A nice illustration of that process has taken place in the US over the last couple of years: that is, in the wake of the crises, legislation was passed which effectively converted the money market mutual fund industry to full reserve. However, the hustlers and shysters managed to get some of that legislation rolled back.

Why we need full reserve banking if it would be more natural if money is printed as much as there are goods, services and other real values in circulation? No more no less. When money is used only as exchange aggregate not as tool to create money out of money (getting something for nothing), then no booms and crises are possible.

Biggest problem in financial system in my mind is that money can be created by private banks and seems that nobody really knows how much money is created and when it will be uncreated. It means that no stability in econoomy is possible as tomorrow all this money can be deleted and we will see crises again.

Let’s just skip the foreplay and go back on the silver standard, which only works incidentally with full reserve banking.